.jpg)

Protein Signals: January clarified where alternative protein is headed

From courtrooms and capital markets to fermentation scale-up, nutrition science, and food policy, January 2026 revealed how the protein transition is shifting from ambition to execution, and where the real constraints are starting to bite

By the end of January, alternative protein no longer looked like a sector waiting to be taken seriously. Across science, policy, infrastructure, and capital, the month showed an industry moving past proof-of-concept and into questions that are harder to answer and more difficult to ignore: cost, digestion, regulation, industrial fit, and political risk.

The stories were not uniformly optimistic. But they were specific, grounded, and increasingly tied to real-world constraints rather than aspiration.

Nutrition moves back to the foreground

Alternative protein research has long emphasized sustainability modeling and theoretical efficiency. In January, nutrition and digestion took more space.

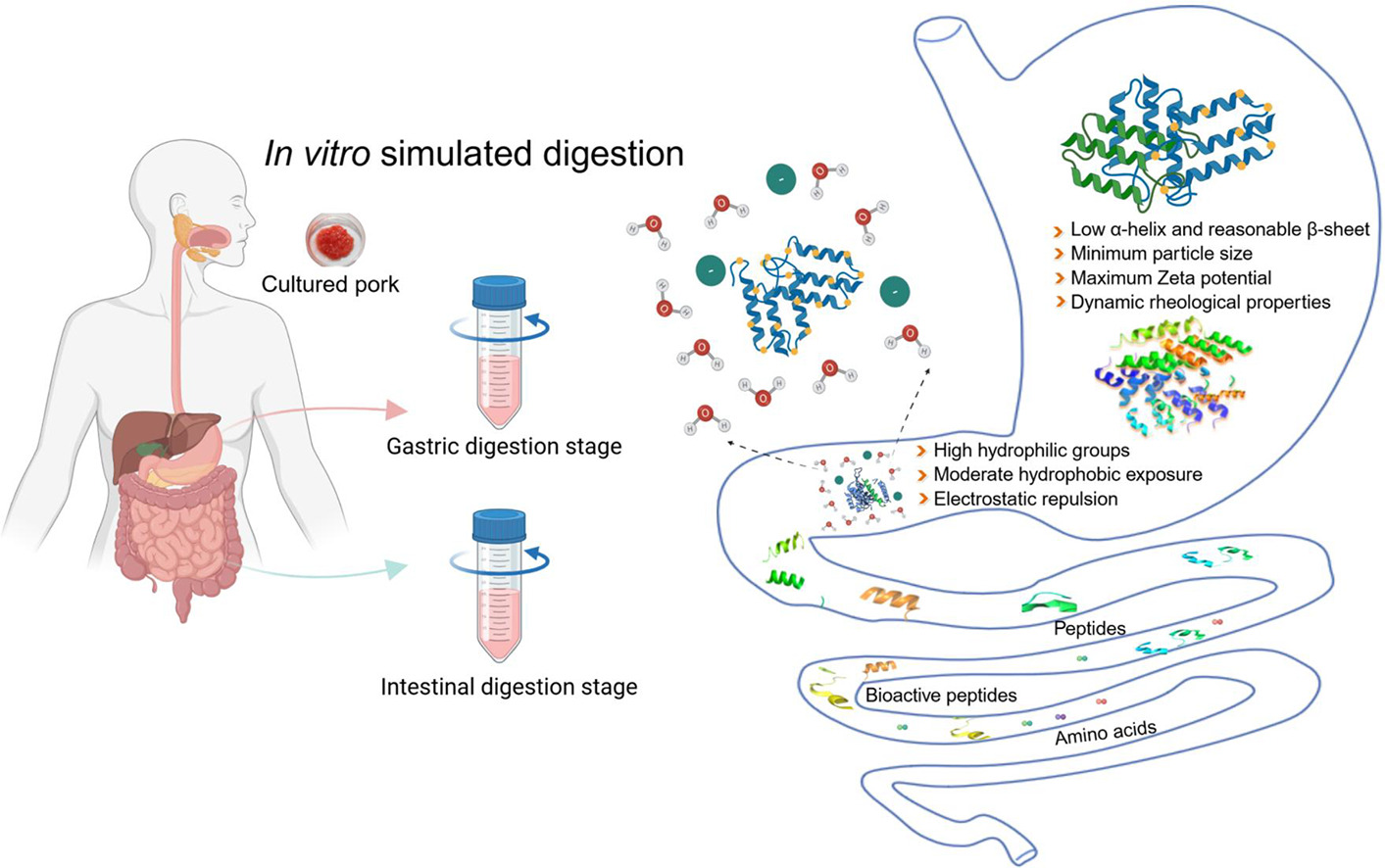

A peer-reviewed study published in Food Chemistry examined how protein derived from cell-cultivated pork behaves during digestion compared with conventional pork, soy, egg, whey, and casein. Led by Yunting Xie at Nanjing Agricultural University, the research used the standardized INFOGEST 2.0 in vitro digestion protocol.

Cell-cultivated pork protein showed higher digestibility during both gastric and intestinal phases than all comparators. It also released higher levels of essential amino acids and generated a greater proportion of small peptides associated with efficient absorption.

Elliot Swartz, Senior Principal Scientist of Cultivated Meat at The Good Food Institute, said the work addressed a long-standing gap. “A common critique of cultivated meat compared to other foods is the lack of knowledge around nutrition and bioavailability,” he said, adding that in vivo studies would still be required.

The findings did not claim nutritional superiority in absolute terms. They added data where little had existed before.

Fermentation-based ingredients followed a similar trajectory. The Protein Brewery secured €2.3 million from the EU LIFE Programme to scale its mycoprotein ingredient Fermotein for dairy alternative applications. The focus was not novelty, but improving nutrition, sensory performance, and cost in a category that has struggled on all three.

“This grant will tremendously accelerate the scaling of our groundbreaking ingredient Fermotein,” said CTO Gilbert Verschelling.

Mycelium ingredient developers took a comparable approach. Maia Farms closed an oversubscribed US$3.75 million seed round to scale mushroom and mycelium-based ingredients positioned as functional tools rather than meat substitutes. CEO Gavin Schneider described the platform as a way to deliver binding, emulsification, and texture alongside protein and fiber.

Across these developments, nutrition and functionality were treated as performance metrics, not marketing claims.

Fermentation consolidates its role

Fermentation occupied a central position throughout January, particularly in Europe.

A report published by Systemiq for The Protein Project concluded that fermentation could become a core pillar of Europe’s protein supply, with political and institutional barriers now outweighing technical ones. Under conservative assumptions, replacing around 3% of animal protein consumption with fermented proteins by 2040 could reduce emissions by approximately 20 million tons of CO₂e annually, alongside substantial land and water savings.

Biomass fermentation was identified as the most immediately scalable pathway, while precision fermentation was positioned as a contributor to hybrid foods and high-value functional ingredients rather than wholesale replacement.

Infrastructure developments reinforced that assessment. GEA was selected to deliver a food-grade precision and biomass fermentation upscaling line for the Biotechnology Fermentation Factory at NIZO’s Food Innovation Campus. The facility is designed to provide open-access capacity at 1,000 and 10,000 liters, targeting the gap between lab-scale validation and commercial commitment.

“Open-access capacity is the critical development link many innovators have been missing,” said Frederieke Reiners, Vice President New Food at GEA.

Digital modeling also moved closer to deployment. New Wave Biotech partnered with Nurasa to integrate bioprocess simulation, techno-economic analysis, and life-cycle assessment into scale-up pathways across Asia. “Scaling biomanufacturing depended on understanding not just how a process behaved, but what that meant for cost, yield and sustainability,” said CEO Zoe Yu Tung Law.

CSIRO and the University of Leeds pursued a similar objective, combining AI and fermentation to convert agrifood waste into microbial protein. The project, backed by the Bezos Earth Fund, aims to determine whether upcycled protein can compete on price rather than sustainability alone. “To truly impact global food security, upcycled protein couldn’t just be a niche alternative,” said Professor Nicholas Watson.

Across these initiatives, fermentation was treated less as an emerging technology and more as industrial capacity under construction.

Cost becomes explicit

January featured unusually direct discussion of production economics.

Planetary disclosed plans to push mycoprotein production below US$1 per kilogram by expanding into India through a potential collaboration with Dhampur Bio Organics. CEO David Brandes said the target was based on operating data from Planetary’s industrial facility co-located with a sugar beet mill in Switzerland.

“The US$1/kg cost target is not based on assumptions, but rather on firsthand production data,” Brandes said.

The strategy relies on integrating fermentation into existing sugar infrastructure to reduce capital intensity, feedstock costs, and energy use. India was identified as a potential low-cost production hub due to sugar side streams, labor economics, and energy integration.

Cultivated meat followed a different economic path but addressed similar constraints. Innocent Meat raised €6 million to advance an automated production system designed for deployment by meat processors using largely standard industrial equipment. CEO Laura Gertenbach said the company was targeting market entry in 2028, subject to regulatory approval.

Investors reinforced the focus on scale and execution. Agronomics injected an additional AU$3 million into All G as it prepared to launch precision-fermented lactoferrin in the US and China. The funding was tied to commercial production, regulatory submissions, and geographic expansion.

Across the month, fewer companies spoke in abstract terms about cost parity. More described specific pathways to reach it.

Policy pressure intensifies

Policy developments in January highlighted how closely protein innovation is now tied to regulation and public decision-making.

In the USA, the release of the Dietary Guidelines for Americans 2025-2030 triggered debate across nutrition and food industry circles. The guidelines emphasized higher protein intake, endorsed full-fat dairy, and urged Americans to reduce consumption of highly processed foods.

Health Secretary Robert F. Kennedy Jr. described the update as “the most significant reset of federal nutrition policy in history.” Critics questioned internal consistency and the treatment of processing, with preventive medicine specialist David Katz pointing to political translation rather than scientific failure.

In Europe, fiscal tools gained attention. A Nature Food study from the Potsdam Institute for Climate Impact Research found that applying full VAT to meat across the EU could reduce diet-related environmental impacts by up to 5.7%, at a net household cost of around €26 per year if revenues were recycled.

Amsterdam moved further, becoming the first capital city to ban meat advertising in public spaces from May 2026. ProVeg Netherlands Director Joey Cramer said the decision aligned climate and dietary objectives, given meat’s emissions profile.

At the same time, researchers warned of economic consequences if transitions are not managed. Another Nature Food study found that up to US$277 billion in European and UK farm assets could become stranded under rapid dietary shifts. “Stranded assets are not just a theory,” said lead author Anniek Kortleve, noting the concentration of investment in livestock and feed production.

The findings underscored the need for policy coordination across agriculture, climate, and industrial transition.

Cultivated meat enters popular culture

Cultivated meat appeared in January not only in policy and courtrooms, but in mass media.

A YouTube video by MrBeast filmed at UPSIDE Foods’ facility surpassed 45 million views, showing how cell-cultivated chicken is produced and including an on-camera tasting. After sampling the product, creator Jimmy Donaldson said, “It tastes just like chicken.”

The video reached an audience largely absent from regulatory or industry discussions. It also arrived after a year in which UPSIDE Foods had focused on litigation and restructuring rather than public visibility.

The legal context remains unresolved. A federal judge allowed UPSIDE Foods and Wildtype’s challenge to Texas’ cultivated meat ban to proceed, keeping the ban in place while constitutional questions move into discovery.

Cultivated meat now occupies multiple public arenas at once: research journals, courtrooms, and mainstream entertainment.

Plant-based settles into maturity

January also challenged claims that plant-based food demand has collapsed.

An analysis published by ProVeg concluded that the market has entered a more selective phase following years of rapid expansion. Flexitarians now dominate demand, prioritizing taste, price, and everyday formats over novelty.

In Germany, plant-based retail sales reached €1.68 billion in 2024. In the UK, volumes declined modestly but remained substantial. Brand performance diverged, with some high-profile players struggling while others expanded.

“The industry is simmering down, not burning out,” said former ProVeg Incubator director Albrecht Wolfmeyer.

Product strategies reflected that shift. Juicy Marbles launched its Umami Burger into 225 Tesco stores, positioned between traditional veggie burgers and highly engineered meat analogs. Mö Foods raised capital to expand oat-based cheese beyond the vegan aisle, targeting everyday consumption rather than niche identity.

Plant-based products did not disappear. They adjusted to tighter consumer expectations.

Join Us At One Of Our Upcoming Events

If you have any questions or would like to get in touch with us, please email info@futureofproteinproduction.com